The Iran conflict is creating a short‑term price shock in global oil while turning North Dakota’s Bakken into a strategically important “pressure valve” for supply, even though local production has been flat to declining in recent months. From the perspective of our team at Proven Realty, that combination of geopolitical risk and regional opportunity is exactly when disciplined, data‑driven decisions about Bakken real estate matter most.

What’s Happening: Iran, Hormuz, and Prices

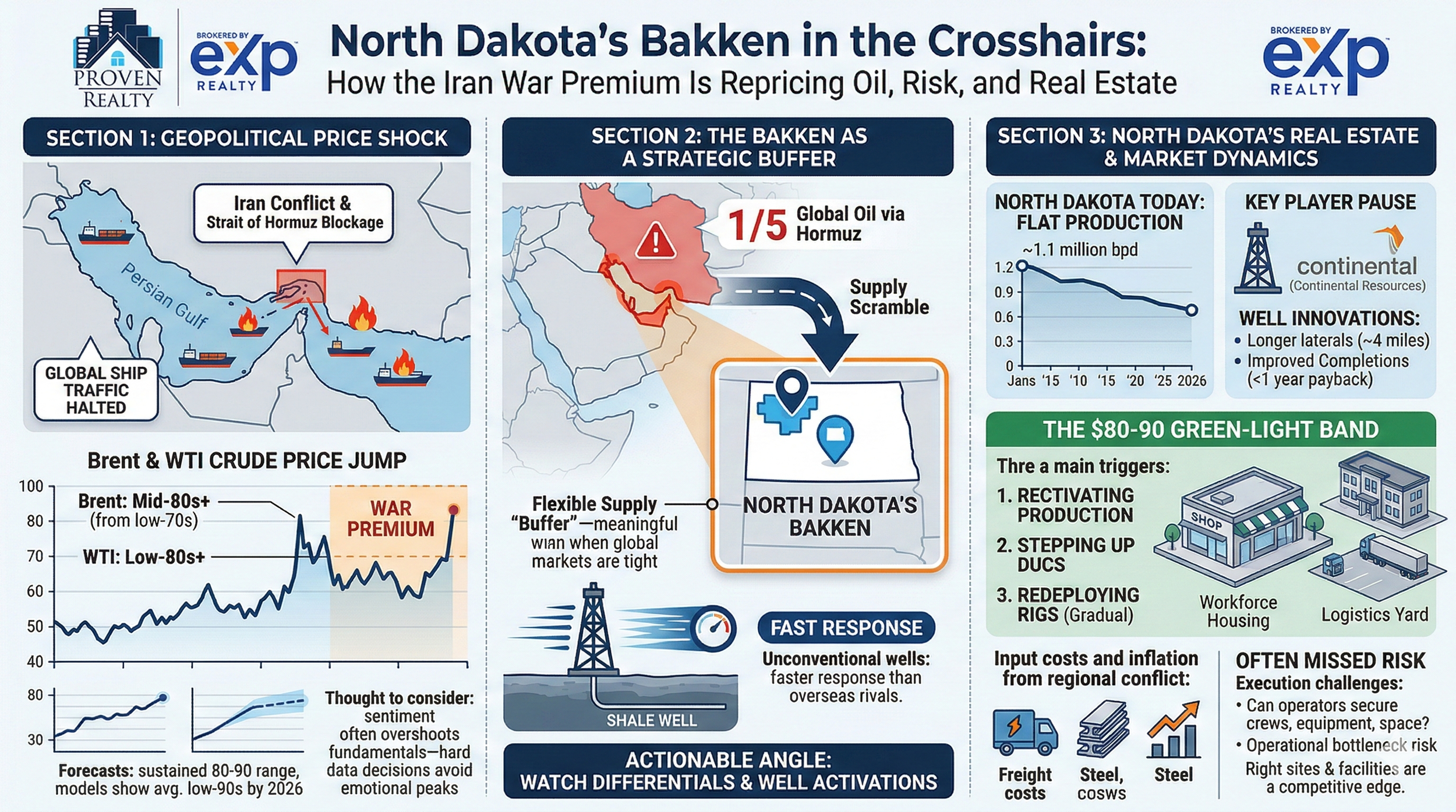

Over the weekend, coordinated U.S. and Israeli strikes hit targets in Iran, with President Donald Trump signaling that a “big wave” of further attacks on Iranian missile, naval, and nuclear capabilities is still to come. Strikes have also extended into Beirut, underscoring that this is a regional confrontation, not a single‑day event. An adviser to Iran’s Revolutionary Guard has threatened that ships passing through the Strait of Hormuz could be set “on fire,” and commercial traffic at this chokepoint has effectively ground to a halt as shippers and insurers pull back.

Brent crude has already jumped into the mid‑80s per barrel and WTI has climbed above the low‑80s, the highest levels since mid‑2024, with trading desks now pricing in a clear “war premium.” Before the latest attacks, Brent closed around the low‑70s with an embedded risk premium of roughly 6–8 dollars, and mainstream forecasts from major banks suggested that a confirmed and sustained closure of Hormuz could keep Brent in the 80–90 range, with some models showing average prices in the low‑90s by late 2026 if Iranian exports and regional transit remain constrained.

Even with this shock, the fundamentals are nuanced: global supply was projected to outpace demand by roughly a few million barrels per day in 2026, which means there is a structural “buffer” that may prevent a 1970s‑style price spike if the conflict does not spread to critical Saudi or Kuwaiti infrastructure.

Thought to consider: in environments like this, sentiment often overshoots fundamentals—those who anchor their decisions on hard data rather than headlines tend to avoid buying at emotional peaks or selling at emotional lows.

Why the Strait of Hormuz Matters – and Where the Bakken Fits

Roughly one‑fifth of the world’s daily oil consumption normally moves through the Strait of Hormuz, so when that artery is threatened or effectively blocked, refiners, traders, and governments immediately scramble to secure alternative barrels. That doesn’t just mean “more expensive gasoline”; it also shows up in shipping and insurance, refinery margins, and government stockpile strategies.

In that context, the Bakken in North Dakota functions as a flexible supply “buffer” rather than a perfect substitute for Gulf exports. Bakken output is on the order of a little over a million barrels per day, a fraction of Hormuz volumes but still meaningful when global markets are tight. Because unconventional shale wells can be completed and turned on more quickly than traditional projects, operators in North Dakota are in a position to respond faster than many overseas competitors once prices justify it.

Actionable angle: investors and operators should be watching not just headline prices, but regional differentials (Bakken vs. WTI), transport constraints, and the pace at which dormant or curtailed wells are brought back online—those are leading indicators of local opportunity and stress.

North Dakota Today: Flat Output in a Spiking Market

Despite the global turmoil and price run‑up, North Dakota has been in a period of flat or slightly declining production. State data show that Bakken output slipped by more than 6 percent between November and December, landing around 1.1 million barrels per day, and regulators had been expecting essentially flat production for 2026. That conservative outlook was built around WTI prices in the 60–65 dollar band, which is roughly the breakeven level for many shale operators once you factor in drilling, completion, and service costs.

Before the recent surge, that pricing backdrop led some key players to hit pause. Continental Resources,

historically one of the anchor operators in the basin, has temporarily stopped deploying new drilling rigs in North Dakota for the first time in about 30 years, citing eroded margins in the low‑price environment, even as it continues to run and optimize existing wells. At the same time, companies have quietly pushed technology forward—drilling longer laterals (sometimes approaching four miles) and improving completions so that many wells can now pay back in well under a year when prices are supportive.

Less obvious consideration: flat basin‑level output does not mean flat local demand for shop space, workforce housing, or logistics yards. Even when rig counts dip, the need for maintenance facilities, laydown yards, and operational bases can remain steady or even grow as operators focus on squeezing efficiency from existing assets.

How an $80–$90 World Changes the Bakken

If WTI sustains above roughly 75–80 dollars, it crosses into what many North Dakota operators view as a “green‑light” band for accelerating drilling and completion activity. With today’s war premium pushing prices into that zone, the basin has three levers it can pull relatively quickly:

Reactivating curtailed production: Wells that were completed but shut in during lower prices can be turned back on with relatively modest capital, providing a fast uptick in output.

Stepping up completions of drilled but uncompleted wells (DUCs): This is the next‑fastest pathway; the rock is already drilled, so capital focuses on fracking and tie‑in.

Gradually redeploying rigs: If high prices look durable, you will see rig counts creep back up after a lag, reversing the recent pullback by operators like Continental.

Offsetting these growth levers are rising input costs tied to broader regional conflict. A prolonged Middle East crisis tends to drive up freight, insurance, and the cost of steel, chemicals, and specialized services used in drilling and completions, which can quietly eat into the margin gains from higher headline prices. A renewed boom would also bring familiar Bakken challenges: tight labor markets, wage inflation, and stress on local housing and infrastructure similar to earlier boom cycles.

Often missed risk: many buyers focus only on the upside of a high‑price cycle and underestimate execution risk—can an operator actually secure crews, equipment, and space in the right locations at the right time? That operational bottleneck risk is exactly where choosing the right sites and facilities ahead of the curve becomes a competitive edge.

Where Erik Peterson and Proven Realty Fit In

Erik Peterson is the founder of Proven Realty and has built his career around North Dakota’s energy‑driven real estate markets, particularly in and around the Bakken. Coming from a real‑estate family and having been active for years in commercial, industrial, residential, and workforce housing projects, he has negotiated over 400 million dollars in transactions across shops, yards, retail, offices, mancamps, and development sites tied directly and indirectly to oilfield activity. That experience extends beyond brokerage into owning and operating Bakken‑based businesses in areas like gravel transport, water and septic hauling, portable sanitation, and real estate development—giving him a ground‑level view of how operators actually use the assets they lease or buy.

Proven Realty is built around that same practical, operations‑first mindset: matching energy companies, service providers, and investors with properties that actually work in a volatile commodity environment rather than just “look good on paper.” The team’s work with planning and zoning departments, engineers, and developers means they are involved from entitlement and design all the way through lease‑up or sale, which is crucial when timelines and costs can swing quickly in response to global events. In a moment when national security planners see North Dakota production as part of the solution to a 20‑percent hole in global seaborne oil flows through Hormuz, that kind of integrated real‑estate and operations expertise helps clients move fast without overreaching.

Key, often overlooked advantage: because Proven Realty sits at the intersection of oilfield operators, local government, and capital, we see early signals—like shifts in planned rig deployments, changes in housing demand from key employers, or new midstream projects—that individual buyers or sellers typically only notice after prices have already adjusted.

Practical Takeaways for Buyers, Sellers, and Operators

For energy‑adjacent investors and operators in North Dakota, this environment is high‑risk but also high‑optionality. A few concrete considerations:

Timing matters more than ever: Jumping in purely because prices spiked on war headlines is rarely wise; targeting assets that remain cash‑flow resilient at 60–65 dollar WTI gives you downside protection if the war premium fades.

Location within the Bakken is critical: Proximity to core drilling areas, major highways, rail spurs, and midstream infrastructure can make the difference between a site that gets used in every price environment and one that only works at the top of the cycle.

Flexibility beats perfection: Industrial shops and yards that can serve multiple types of operators—E&P, midstream, construction, logistics—tend to hold value better across volatile cycles than highly specialized single‑use facilities.

Housing strategy needs a cycle view: Workforce housing and residential assets in oil country can be very attractive in a boom, but designs and locations that appeal to both oilfield and non‑oilfield tenants are more resilient when activity slows.

What we emphasize at Proven Realty is structuring deals to survive both the war‑premium spike and the return to fundamentals: lease terms, escalation clauses, and contingency planning that assume prices could retrace even as geopolitical risks remain. That kind of structure is what separates speculative bets from durable positions that benefit from the Bakken’s growing strategic importance without being hostage to every headline.

Sources:

CNN live coverage and analysis of U.S.–Israel–Iran conflict and Strait of Hormuz disruption, March 2026.

CNN: “Oil surges and stock futures sink after war in Iran disrupts crude supply.”

CNBC: “Oil soars amid Strait of Hormuz shipping fears as Iran war drives prices to nearly $80.”

BBC: “Oil and gas prices jump and shares fall as conflict escalates.”

Continental Resources Bakken drilling pause and North Dakota production context.

Erik Peterson and Proven Realty background.